20 Mar 2017

Help to Buy – A fantastic way to get on the property ladder!

Mortgage Required are approved Help to Buy Mortgage Advisers and have helped lots of clients to buy a home through this government fantastic scheme.

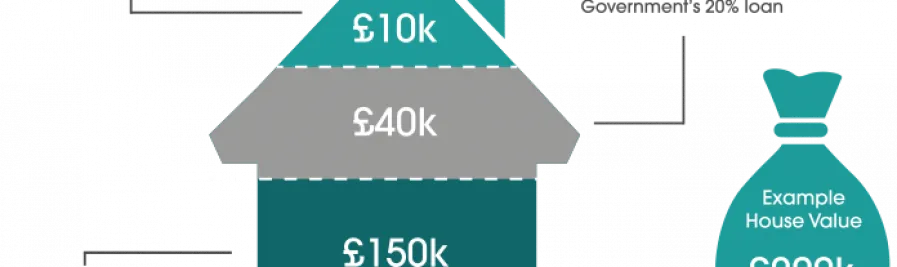

With a Help to Buy: Equity Loan the Government lends you up to 20% of the cost of your newly built home, so you’ll only need a 5% cash deposit and a 75% mortgage to make up the rest.

You won’t be charged loan fees on the 20% loan for the first five years of owning your home.

If the home in the example above sold for £210,000, you’d get £168,000 (80%, from your mortgage and the cash deposit) and you’d pay back £42,000 on the loan (20%). You’d need to pay off your mortgage with your share of the money.

But… what happens if property values fall?

When you sell your home, (unless you have repaid the Help to Buy equity loan document previously) the Help to Buy equity loan document commits you to repay a percentage of the market value equal to the percentage contribution of assistance received.

This means if the market value of your property falls below the level at which it was first purchased, you will repay less than the original amount the Agency contributed to the original purchase.

Here are the key features of the Help to Buy scheme:

| Amount of loan | The maximum you can borrow from Help to Buy in England is £120,000 and up to £240,000 for London. There is no minimum amount. |

| Buyer deposit required | Buyers must provide a deposit of a minimum of 5% of the full purchase price of the home bought under this scheme. |

| Maximum Purchase Price | £600,000 |

| Frequency, number and amount of repayments |

After five years you will be required to pay interest of 1.75% of the amount of your Help to Buy shared equity loan. This rises each year by the Retail Prices Index (RPI) plus 1%. The loan itself is repayable after 25 years or on the sale of the property if earlier. |

| Other payments and charges | You must pay a monthly management fee of £1 per month from the start of the loan until it is repaid. |

| Total amount repayable |

Total amount repayable The total amount repayable by you will be the proportion of the market value of your home that was funded by this loan, plus interest and charges. The amount you will have to repay under the loan agreement will depend on the market value of your home when you repay the Help to Buy equity loan and the rate of inflation in the meantime. |

To speak to one of our Help to Buy experts, please give us a call on 01628 507477.

Recent posts

Here are the lowest fixed mortgage rates of the week, available to first-time buyers, home movers, buy-to-let, and those remortgaging.

Call us for more information: 01628 507477 or email: team@mortgagerequired.com.

Andy Burnham’s Potential Changes

8 days ago

Despite the Prime Minister not yet announcing any policies to abolish or change Stamp Duty, speculation persists that this could become government policy.

Burnham, who officially became Prime Minister on Monday, 20th July, has expressed strong support for a significant reform of property taxes over recent years. He said that he will deliver “the most significant change moment in our politics for 40 years.”

Young borrowers concerned about credit score

23 days ago

Almost half of young adults are worried about their credit history stopping them from renting or buying a property, according to data from Loqbox

How to add value to your property this summer

26 Jun 2026

Different seasons can have a noticeable effect on property prices.

Research from Zoopla shows that spending out on certain features can fetch up to £29,000 during the summer months.

Monday 22nd June saw Keir Starmer resign as Prime Minister and Labour leader. The resignation does not directly impact mortgage rates, as changes were taking place before this announcement. However, it could influence mortgage rates indirectly through financial markets and future government policies.

Homebuying reform to cut homebuying times by around four weeks, and save first-time buyers around £650, says the government.

Buying your first home is a huge milestone, but it can also be a complex process. There are several factors a first-time buyer should consider before making an offer on a property, including understanding the difference between leasehold and freehold and checking council tax bands.

We’ve detailed some questions you can ask your estate agent to help you make an informed decision.

Signs it's time to remortgage

17 Jun 2026

Remortgaging means switching to a new mortgage deal. This will either be with your current lender or a new one.

Getting advice and moving to a new deal when the time is right can mean lower monthly mortgage payments, better interest rates, or releasing equity from your property.

Here are some signs it may be time to remortgage.

More information

Trusted by