It looks like the Government’s Help to Buy 2 scheme will come to an end on 1st January 2017 as planned.

For those of you who get a bit muddled about which help to buy is which, it’s basically the one where the Government acted as guarantor to mortgage lenders to enable them to lend 95% mortgages, post credit crunch.

I don’t think there is anything really to worry about here, a lot of lenders have quietly moved away from Help to buy 2, preferring to lend their own funds which is clearly more profitable for them. Of course the applicant never knows if their particular scheme is government backed or not, all they need to know is “Are there 95% funds available.”

The answer to this post H2B2 is most certainly going to be “Yes.” Santander, Halifax, Accord, Nationwide, and Newcastle Building Society have all announced that they will be offering 95% mortgages in 2017. Other lenders are yet to announce their positions.

All lenders are more risk averse post credit crunch (and possibly post Brexit), but a first time buyer with a 5% deposit who manages to get through the lender’s credit score ticking every “responsible lending” box along the way, would seem like a pretty safe bet to me.

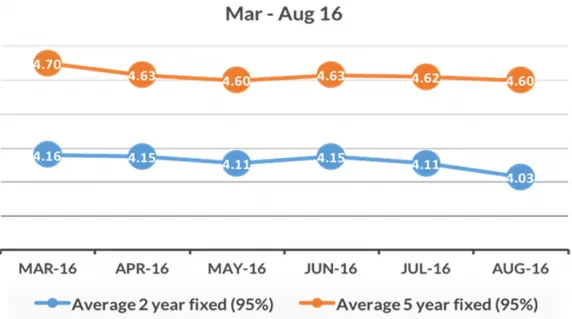

The number of available 95% products available remains significantly higher than in 2015 and the interest rates on offer have fallen recently.

My advice to anyone saving for their first home is to open a Help to Buy ISA account TODAY! This is the best place to save for your deposit as the government will give you some money to boost your savings.

Once you have got the government boost and exhausted the Bank of “Mum & Dad, ” if you only have a 5% deposit I am pretty sure there will be a lender with a competitive rate ready to receive your application.

Related Blog articles:

For more information speak to a mortgage adviser on 01628 507477 or contact us .

Recent posts

Best UK Mortgage Rates this Week

2 days ago

Here are the lowest fixed mortgage rates of the week, available to first-time buyers, home movers, buy-to-let, and those remortgaging.

Call us for more information: 01628 507477 or email: team@mortgagerequired.com.

Andy Burnham’s Potential Changes

10 days ago

Despite the Prime Minister not yet announcing any policies to abolish or change Stamp Duty, speculation persists that this could become government policy.

Burnham, who officially became Prime Minister on Monday, 20th July, has expressed strong support for a significant reform of property taxes over recent years. He said that he will deliver “the most significant change moment in our politics for 40 years.”

Young borrowers concerned about credit score

25 days ago

Almost half of young adults are worried about their credit history stopping them from renting or buying a property, according to data from Loqbox

How to add value to your property this summer

26 Jun 2026

Different seasons can have a noticeable effect on property prices.

Research from Zoopla shows that spending out on certain features can fetch up to £29,000 during the summer months.

Monday 22nd June saw Keir Starmer resign as Prime Minister and Labour leader. The resignation does not directly impact mortgage rates, as changes were taking place before this announcement. However, it could influence mortgage rates indirectly through financial markets and future government policies.

Homebuying reform to cut homebuying times by around four weeks, and save first-time buyers around £650, says the government.

Buying your first home is a huge milestone, but it can also be a complex process. There are several factors a first-time buyer should consider before making an offer on a property, including understanding the difference between leasehold and freehold and checking council tax bands.

We’ve detailed some questions you can ask your estate agent to help you make an informed decision.

Signs it's time to remortgage

17 Jun 2026

Remortgaging means switching to a new mortgage deal. This will either be with your current lender or a new one.

Getting advice and moving to a new deal when the time is right can mean lower monthly mortgage payments, better interest rates, or releasing equity from your property.

Here are some signs it may be time to remortgage.

More information

Trusted by